Vallianz Sukuk Demonstrates Much Needed Cross Border Tapping of Islamic Capital Markets

Vallianz Holdings issuance demonstrates much needed cross border Islamic capital market activity.

The Vallianz sukuk was issued through its Saudi Arabia based Rawabi Vallianz Offshore Services Limited (RVOS) unit of which it is a 50% shareholder. The sukuk issued in Saudi Arabia and denominated in Saudi Riyals for a value of SAR1 billion is a five year issuance and was arranged by a number of Saudi based banks.

Vallianz had announced late last year it intended to refinance using sukuk with the structure involving the transfer by RVOS Vessels for an aggregate consideration of approximately US$410.0 million into a SPV which would then lease back for a term of five years in return for quarterly charter rates to cover financing obligations. Loans were also transferred into the SPV and refinanced.

IILM and Kuwait Finance Issuances

The Malaysian based International Islamic Liquidity Management Corporation (IILM) also issued as part of its regular short-term sukuk issuance programme a $1.34 billion sukuk at a profit rate of 1.038% to mature on 24 May 2016. The sukuk was oversubscribed with total bids received of $1,661 billion.

The Turkey based unit of Kuwait Finance House issued a $350 million sukuk at a profit rate of 7.9%. The Fitch BBB- rated sukuk was issued with a 10 year maturity in order to boost the Turkey based unit’s Tier 2 capital ratio and will be listed on the Irish Stock Exchange.

There has been a growing interest in the past few years towards socially responsible investment (SRI) sukuk or green sukuk. A number of sukuk in this class has been issued in the global market to finance environmental-friendly projects.

The growing trend toward SRI sukuk or green sukuk is mainly due to the natural progression of sukuk market, the growing awareness of investors toward ethically and socially responsible investment and the stricter capital requirements for the bank to finance infrastructural projects. This report looks at the future of SRI sukuk or green sukuk as well as the challenges surrounding its growth.

The New Era for SRI & Green Sukuk

There has been a growing interest in the global market toward SRI instruments. One of the areas that are normally associated with SRI is the environment and its preservation. Green bond therefore becomes a common instrument to serve this aspect of SRI in the global market. For example, in 2007 the European Investment Bank (EIB) launched a EUR 600mln climate awareness bond focusing on renewable energy and energy efficiency.

Subsequently in 2008, World Bank issued a total of USD440mln green bond to support climate-focused program for the Scandinavian pension. In 2013, the African Development Bank issued a USD500mln green bond to finance climate change solution in Africa. As of June 2015, the World Bank has issued over 100 green bond papers valued at USD8.5bln. To date, there is approximately USD65.9bln worth of green bonds available in the market.

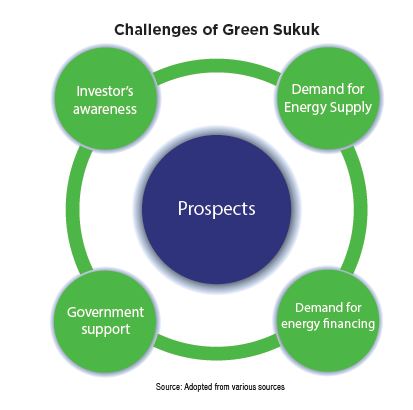

Challenges of Green Sukuk

Challenges

Not withstanding the positive prospects for green sukuk, the future of green sukuk is hindered by a number of challenges and constrains. First, the secondary market for green sukuk is very small due to small number of investors holding sukuk funds and other institutional investors which traditionally require robust secondary market for meeting the investors’ liquidity expectations. Second, the absence of the standard and verification system for performance measurement of green bonds/sukuk. Third, green sukuk may expose to higher risk profile. This is because many environmental friendly projects involve a sophisticated degree of new technology due to construction and operation of green technologies. Fourth, the difficulty to assure investors that sukuk proceeds will be used for projects with economic value, while meeting accepted and credible green standards.

Commentary by RHB Global Sukuk Markets Research, Kuala Lumpur, Malaysia

The Bloomberg Malaysia Sukuk Ex-MYR Total Return (BMSXMTR) and Dow Jones Sukuk Total Return (DJSUKTXR) indices closed slightly higher at 101.0 (+0.19%) and 153.5 (+0.36%) respectively, with weighted average yield declined 2.5bps WoW to 2.81%. SECO ’22-24 and Qatar ’18-23 gained by USD86.6m in market cap but partially offset by RAKS ’25, SHARSK ’24, NOORBK ’20, PETMK ’20 and QIIK ’17.

Brent oil has been trading in volatile range that finally settled 6.8% higher WoW to USD30.5/bbl. However, prospects remain weak on subdued demand in China and oversupply condition persists following re-entry of Iran, Iraq’s highest production December (of 4.13m bpd) and National oil Saudi Aramco’s to maintain capex plan despite gap between supply and demand were about to narrow in 4Q15 (see Chart of the Week), according to EIA. Focus this week would be on US FOMC meeting, ECB and BOE (tonight) as well as BoJ on Friday. Malaysia will announce their Budget revision on Thursday (28 Jan)

Sharjah (A3/A/NR) printed USD500m of 5y Sukuk at MS+250, which carries a profit rate of 3.839%, while Exim Bank Malaysia (A3/NR/NR) printed a USD37.3m of 5y at 3.01% last week. In the pipeline, Oman Telecom and Gulf Investment Corp (GIC) are among issuers eyeing for sukuk deal, apart from Indonesia, Khazanah and TNB.

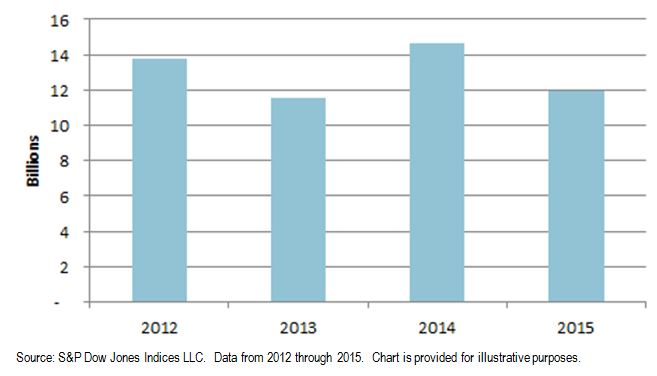

The big under performers of the index were Saudi Electric, and the sovereign sukuk issued by Bahrain and South Africa. 15 new sukuk with a total par amount of USD 11.95 billion were added into the Dow Jones Sukuk index, of which 48% were from the Middle East and North Africa (MENA). Strong demand was displayed for the Malaysian Sovereign sukuk issuances, with strong order books of two-to-three times oversubscribed.

Exhibit 1: Total Par Amount of New Sukuk Issuances

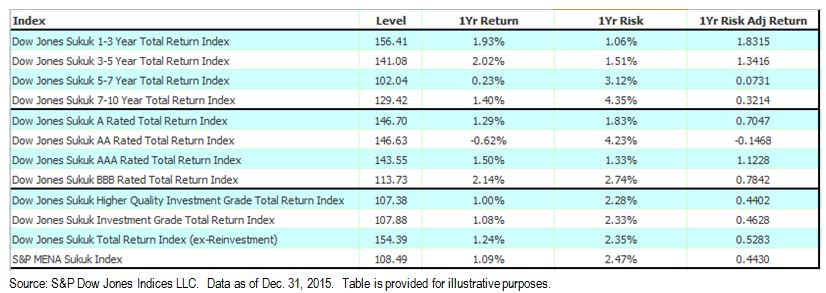

Exhibit 2: Performance of the Dow Jones Sukuk Index Family in 2015

The Programme, while backed by the credit of ICD as obligor, was established with Hilal Services Ltd, a Cayman Islands incorporated SPV, as the issuer. The first public issuance under the Programme will represent ICD’s first public fund raising in the debt capital markets and will follow the example of its parent The Islamic Development Bank which has a US$10 billion Sukuk Issuance Programme.

The Reg S fixed rate resettable tier 2 sukuk is due 2025 and is backed by the credit of Albaraka Turk as obligor, was issued by Albaraka Sukuk Ltd.

The sukuk will pay a profit rate of 891bps over the five year US dollar mid swap rate and represents Albaraka Turk’s third international sukuk issuance following the issuance of their tier 2 sukuk in 2013, and their senior sukuk in 2014.

Gregory Man, partner in the Dubai office for Norton Rose Fulbright , commented: “We were pleased to be able to assist Albaraka Turk in executing this transaction in order to add to their capital base. This is only the second Basel III compliant tier 2 deal to come out of Turkey, and the first in sukuk format. The transaction represents another landmark deal in the Turkish market and builds on our firm’s growing reputation in Turkey.”

Clifford Chance LLP also advised Deutsche Trustee Company Limited as Delegate. Maples and Calder provided Cayman law advice.

Eleven Bids were received for value of $643 million resulting in a fully subscribed $490 million issuance by the Kuala Lumpur based International Islamic Liquidity Management Corporation (IILM). The IILM is an industry body which provides highly rated liquidity within the Islamic Banking and Capital markets.

The $490 million reissuance marks the 21st series of short-term IILM Sukuk, rated A-1 by Standard and Poor’s Rating Services. As at November 2015, the IILM Sukuk that have been issued and reissued amount to USD13.18 billion.

The reissuance marks the 21st series of short-term IILM Sukuk, rated A-1 by Standard and Poor’s Rating Services. The reissuance was fully subscribed by the following primary dealers (in alphabetical order) who participated in this auction:

1. Abu Dhabi Islamic Bank;

2. Al Baraka Turk;

3. Barwa Bank;

4. Boubyan Bank;

5. CIMB Islamic Bank Berhad;

6. Kuwait Finance House;

7. Maybank Islamic Berhad;

8. National Bank of Abu Dhabi;

9. Qatar Islamic Bank;

10. Qatar National Bank; and

11. Standard Chartered Bank.

As at November 2015, the IILM Sukūk that have been issued and reissued amount to USD13.18 billion.

Tose’e Melli Mining and Industries Company is raising 1.62 trillion rials ($45.8 million at market exchange rate) through the first-ever sale of Estensa (Istisna) Sukuk on the Tehran Stock Exchange.

The domestic deal which is planned for Nov. 23 was reported in Iran as paying 23% profit annually with a three year maturity for the purpose of raising funding for two iron ore concentrate and pellet plants.

Standard & Poor’s Ratings Services has assigned its preliminary ‘B’ issue rating to the proposed $350 million Tier 2 sukuk trust certificates to be issued by Albaraka Sukuk Ltd. Albaraka Sukuk (the issuer) is a special-purpose vehicle incorporated in the Cayman Islands.

It will enter into sale and purchase agreements and a Murabaha agreement with Albaraka Turk Katilim Bankasi (ABT; BB/Negative/B), a participation bank incorporated in Turkey. The sale and purchase agreements (51% of the issuance amount) are for a diversified portfolio of Sharia-compliant assets. The Murabaha agreement (49% of the issuance amount) is for a portfolio of commodities.

Robert Pakpahan, director general of the Indonesian Finance Ministry said his office expected to boost the proportion to 30 percent of total gross bond issuance, an increase from around 24 percent in 2015.

In 2015 alone, the government generated more than Rp 350 trillion (US$25.83 billion) from the domestic market, and has so far sold US-dollar bonds in the global and domestic markets, US-dollar global sukuk (Islamic bonds), euro-denominated bonds in Europe and samurai or yen-denominated bonds in Japan.

Data and information provided on this site is not warranted, it maybe incorrect and/or incomplete. By continuing to browse this site you are accepting to our use of cookies and that information provided is not warranted.